Can I Buy a Home with Student Loan Debt?

According to the US Department of Education, nearly one-sixth of American adults are riddled with student loan debt, which now tops around $1.6 billion nationwide. It’s no surprise then that many individuals feel they aren’t prepared for the expenses involved with becoming a homeowner.

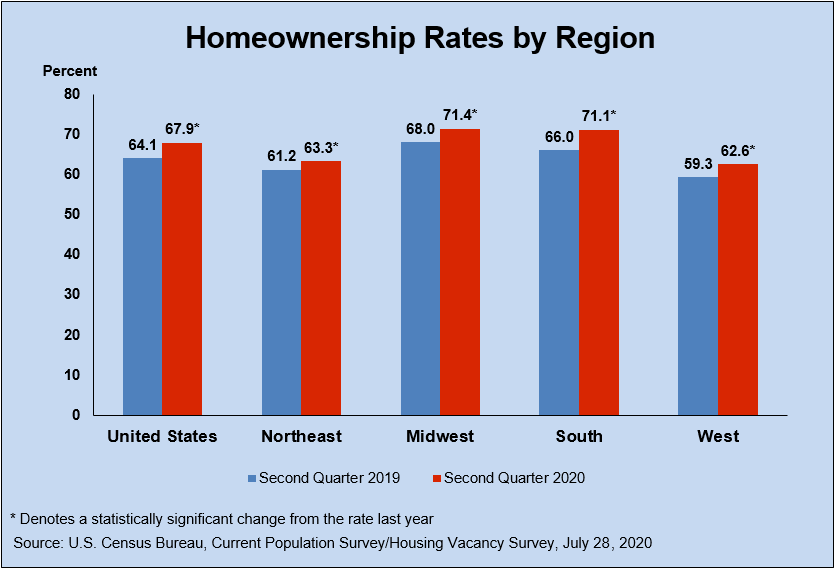

This is especially true of the millennial generation, of which just 38% own their own homes. This is a stark contrast to the overall homeownership rate of nearly 68% among Americans as a whole. This disparity is largely due to the financial burden student loans have created for young adults who chose to further their education.

With standard student loan repayment plans costing $200 to $300 per month on average, it can seem daunting to tack on the responsibility of a mortgage payment to your monthly expenses. However, it’s worth noting that the cost of owning a home may be more affordable than renting, especially when interest rates are lower. Below, we’ll explore your options when it comes to buying a home with student loan debt and how it could be a smart financial move.

{kind=link}

How to Buy a Home with Student Loan Debt?

1. Build Your Credit

The number one thing you can do before buying a home, whether you have student loans or not, is improve your credit. If you have a short credit history or some negative marks on your credit, it’s important to build your credit in order to qualify for a mortgage. A conventional loan is more forgiving to prospective borrowers with student loan debt than other loan programs. We also have access to excellent low to no down payment options. However, in order to qualify you’ll still need to have decent credit.

2. Decrease Your Overall Debt

Easier said than done, especially when you have student loans accruing interest. If you can focus on paying down other debts (such as credit cards, auto loans, etc.) while simultaneously paying your monthly student loan payment, it will be very beneficial for lowering your debt-to-income (DTI) ratio when it comes time to apply for a mortgage.

3. Consider First-Time Buyer Programs

If you are considering making the leap to homeownership, it’s a good idea to talk to a C&F Mortgage industry expert and see what loan programs are available to you. Many first-time loan programs have lower credit score and down payment requirements, which may be helpful if you’re juggling student loan debt and trying to save up for your down payment on a home. Keep in mind that your student loan debt will be a determining factor when going through the mortgage approval process, so it’s a good idea to bring that up early on in the conversation to see which programs are best for you.

4. Refinance for Greater Affordability

If you already own a home and you have student loan debt, you may be able to consolidate your debts into a single monthly payment by refinancing your student loans into your mortgage. This could make your monthly obligations much more affordable since you’d be spreading your payments out over a longer period (15 or 30 years for a mortgage vs. 10 years for student loan repayment). This option may not always make sense financially, but it could reduce your overall student loan interest quite a bit by consolidating your debts.

No matter where you’re at on the journey to homeownership, C&F Mortgage is focused on you every step of the way. Get in touch with one of our local industry experts today to see how you can make buying a home a reality while repaying your student loans.

Edited 6/20/2023. The information contained herein (including but not limited to any description of C&F Mortgage Corporation and its lending programs and products, eligibility criteria, interest rates, fees and all other loan terms) is subject to change without notice. Restrictions apply. This is an advertisement and not a commitment to lend. C&F Mortgage Corporation NMLS# 147312 Equal Housing Lender.